Adulting - Our Annual Budget Review

Adulting - Our Annual Budget Review

How we are saving over $25,000!!! Say what?

As I’ve previously mentioned, we’ve been trying to max out our retirement savings every year and then save even more on top of that. We want to retire one day (sooner rather than later). One of the things we do each year to help with this process is to review our annual expenses and look at areas we are overspending or things we can cut from our budget. We typically do this in January and then a mid-year check-in. When we were in the debt paying off stage of our life we had monthly family budget meetings (and yes, we’ve always included the kids in these - we feel its really important for them to know what the real world/adulting costs). This also helps us set family priorities aligned with our values (more trips and experiences and less stuff).

One of our largest expenses each month to date (right behind our mortgage) has been our health insurance. We have been hesitant to switch from our private, grandfathered-in health insurance plan as it allows us to see doctors anywhere (BUT - it kept going up in price to the tune of $2200/month next year - this is not one of the perks of owning our own small business). So we spent days looking at ACA plans and other private insurance plans and small business plans, etc. and they were all just as expensive for us but with less coverage &/or higher deductibles. So we made the leap to a medical cost-sharing plan. We’ve heard good things about this one (Dave Ramsey even recommends it) and it is saving us $1297 a month. We may have a few more out of pocket expenses for things like annual checkups, annual mammogram, etc. but the BIG stuff (ER visits, surgeries, etc. are for the most part covered).* Please note there are a lot of exceptions for this including pre-existing conditions, etc. so please do your research to see if this is a good fit for your family. When signing up they also wanted to know what church we go to and there was a fair amount of Christian value wording in their policy (not a super fan of some of it as you can imagine) but our priority was covering our family in the event of severe medical needs beyond well-child check-ups and this seemed like the most affordable (and kindest) way of doing it. Think of it as a giant pool of money for medical bills that you hope you never have to draw from despite contributing to it monthly. Anyway, we’re going to give it a go this year and see how it works.

Okay so here is what else we did to save some mega bucks this year.

Switched from a Health insurance private plan to Christian Cost Sharing Plan $2,068/month to $771/month. Saving $15,564/year

Switched phones from Verizon to Visible. $267 to $100/month. Saving $2,004/year

Switched providers for Flood Insurance ($3280/year to $635/year). $2,565/year in savings. Why we didn’t do that 15 years ago I DO NOT KNOW.

Let go of our 2x/month house cleaning help :( I miss her terribly but living in a smaller space it just didn’t make sense. ($500/month to $0/month) - $6,000 a year in savings.

Stopped Peloton Subscription ($48/month to $0) we can still ride it just without the classes ($480/year in savings). Although we are contemplating getting a family membership at a nearby gym & selling the peloton - my home half ass workouts aren’t cutting it anymore - more on this potential monthly expense in a future post and how I will consider it a HEALTH CARE expense in the budget.

Bundled our auto & home insurance and are saving $789/year.

No more orthodontist bills (both kids have straight teeth and I decided against doing Invisalign for now) $2,628/year in savings (we’ve had over 4 straight years of orthodontist bills). We also discovered we were overcharged accidentally $1802 by the orthodontist (auto billing was never turned off once the full amount was paid, so we will be getting a $1802 check back). It’s important to keep track of your bills, people! ;)

ps - All of our travel happens due to points rewards thru our fav credit card (which we pay off in full each month). We prioritize travel as a family - adventure is one of our core values. One way we do this is to save up our travel miles that we get using our credit card (we have one for personal and one for business expenses). Please note if you have credit card debt or have a difficult time paying off your credit cards each month, I do not recommend you get another credit card. But if you are capable of spending mindfully and paying it off each month in full, then credit cards can be a great way to rack up travel points (if used judiciously). I also use this shopping link to save money - it automatically applies coupons/discounts when using our credit card.

Also, we do have some additional expenses this year including college tuition, travel expenses to a few family events, a new electric vehicle (that we’ve been saving up for, for 3 years), etc. Our auto insurance is also going to go up once we have the EV and once we have another kid driving. Eek. Anyway these are things we make note of in our annual budget talks.

I hope this helps you dive in and maybe cut some costs from your budget too.

ps - Here are some previous posts about our financial freedom goals & budgeting in case you missed them.

Okay, so what are you doing to save $$$? With talks of recession looming again and student loan payments resuming, and mortgage rates high, saving money is on all our minds.

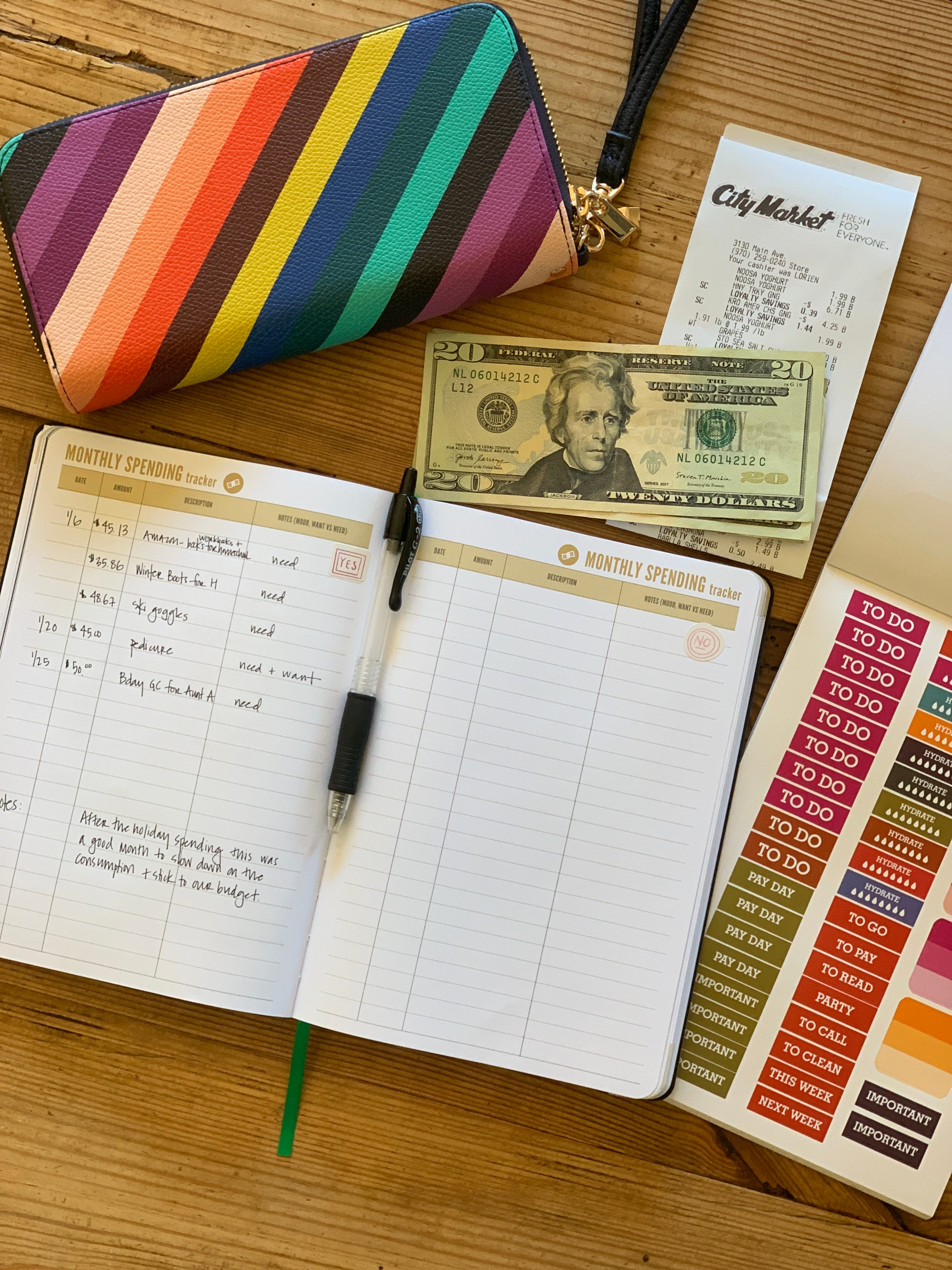

Commit30 Money Journal pictured above. This helps me track our spending each month and notice areas where we are over-spending. I know there are lots of apps that do this but there’s something about actually writing in the amount you spent that is critical.

Disclosure of Affiliate Links: Some or all of the links in this resource list are affiliate links. This means if you click on the link and purchase the item, I will receive an affiliate commission and we are disclosing this in accordance with the FTC. Please know that I want to encourage you to use what you already have. When I suggest products or companies, I only share items that I use and recommend. Having said that purchase at your own risk.